Today’s column continues consideration of the likely cost-price relation that might be anticipated during Guyana’s coming time of oil and gas production and export. So far, the discussion has established both indicative cost and indicative price estimates for Guyana’s oil circa 2025.

It has also strongly argued: 1) 2025 is too far out into the future, and 2) the oil and gas markets are much too volatile for anyone (including me) to provide estimates, which are significantly superior to informed guesses! I have further, urged readers to keep this caution constantly in mind, particularly as several ‘market analysts’ and high-reputation institutions churn out such estimates with regularity. Often these betray, to those who follow them closely, a high frequency of estimation errors.

Despite this caution, it is reasonable to posit that the present consideration of such matters is not premature for Guyana.

It certainly directs readers’ attention to some of the most crucial considerations which should engage meaningful contemplation of Guyana’s prospects in its coming time of oil and gas production and export.

Today’s column specifically addresses the notion of the break-even price for crude oil, as seen by its producers. This notion is central to the sustainability and commercial viability of Guyana’s operations, as indeed, would be the case for any business enterprise.

Break-even price

In economics, business and finance the break-even price is known as that price where the total cost of operating a business is just equal to the total revenue obtained by that business from its sales. The cost that is referred to here is opportunity cost. Opportunity cost is also known as economic cost. It is formally defined as the ‘next best forgone alternative that was not chosen’ for those resources used in a business.

It is important to stress that, in this sense, investors get a return based on (derived from) the risk-adjusted next best earnings they could obtain for the funds they put into the business.

This is sometimes known as normal profit. It can also be described as the amount of accounting profit, when the economic profit is zero.

In practice, the break-even price is one of the most frequently used concepts in business and economic analysis. Economists, however, emphasize, this is not a generic price.

That means this price varies with the type of business for which it is being constructed. The break-even price of crude oil is therefore developed as a measure specific to the crude oil industry. For the Guyana environment certain features of its crude oil industry would stand out when seeking to establish its break-even price.

First, Guyana would be a price-taker and not a price maker in the future global crude oil market.

At present, even some of the largest producers (operating as a cartel through OPEC), do not have enough market power to fix the price or even a price range in the crude oil market that is acceptable to major non-OPEC market players. This is especially true for those non-OPEC players with considerable global geo-strategic weight, namely, the United States, Russia, China, Japan and India. Second, Guyana’s projected daily or annual output levels are likely to account for only a small fraction of global sales over the short to medium term of its existence.

Importance

Knowledge of the break-even price is useful to the producers (exporters) of Guyana’s oil and gas industry for several reasons including 1) ensuring there is an established benchmark for rating its competitiveness; 2) serving as a marker for guiding Guyana’s market share strategy; 3) deciding on the expansion path for Guyana’s oil and gas production; 4) measuring the productivity of Guyana’s operations; 5) establishing global comparators of cost competitiveness and efficiency level; and 6) supporting market and pricing policies that would favour Guyana.

The gap between the crude oil break-even price and the prevailing market price serves as an indicator of the margin of safety for Guyana’s operations. The wider the gap between current output and the break-even level of output, the greater is the margin of safety for Guyana’s operators.

At this stage we can say with some certainty that the key costs facing Guyana’s operations would be as shown in Schedule 1. These costs are frequently classified by oil firms as fixed and variable costs.

Variable costs refer to those costs that change with the level of production and distribution (for example transportation and most wages). Fixed costs are those that change with changes in the level of production (for example new oil wells and production platforms).

Break-even costs

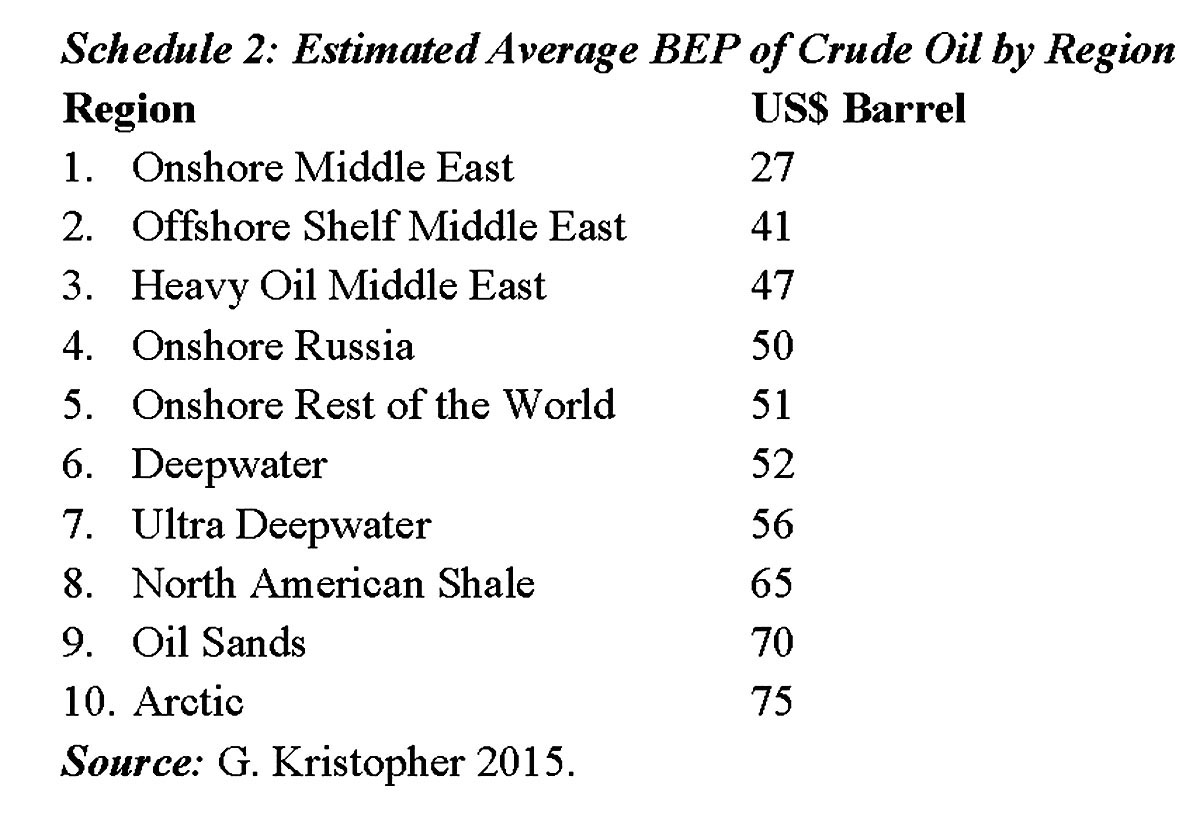

To provide readers with some idea of typical break-even prices across various regions, I provide in Schedule 2, G Kristopher’s estimates of break-even price for crude oil production for ten broad regions. The regions’ estimates are calculated as averages of prices within each region.

The range in these data is striking. The highest break-even price estimate (for the Arctic Region @ US$75) is 2.8 times more than the lowest break-even price estimate (for the Middle East Onshore @ US$27). The average of the break-even prices cited is US$53 per barrel.

Conclusion

Next week I advance this discussion by introducing the concept of the fiscal break-even price for crude oil, as distinct from the break-even price as seen by the industry’s investors and operators, which has been covered here so far.

Dr Clive Thomas

November 13th, 2016

Original Source: https://www.stabroeknews.com/2016/features/11/13/guyana-oil-break-even-price/