Introduction

Today’s column furthers the discussion of the fiscal break-even price for crude oil. As previously indicated, this is a normative price, which is dependent on what governments figure that price ought to be, if they are to obtain the level of revenue that they need from oil to meet their expected spending requirements, while maintaining a balanced budget.

Because of this expectation, one would further expect that, as a rule, the fiscal break-even price for crude oil would tend to be higher than the break-even price generated by commercial market factors.

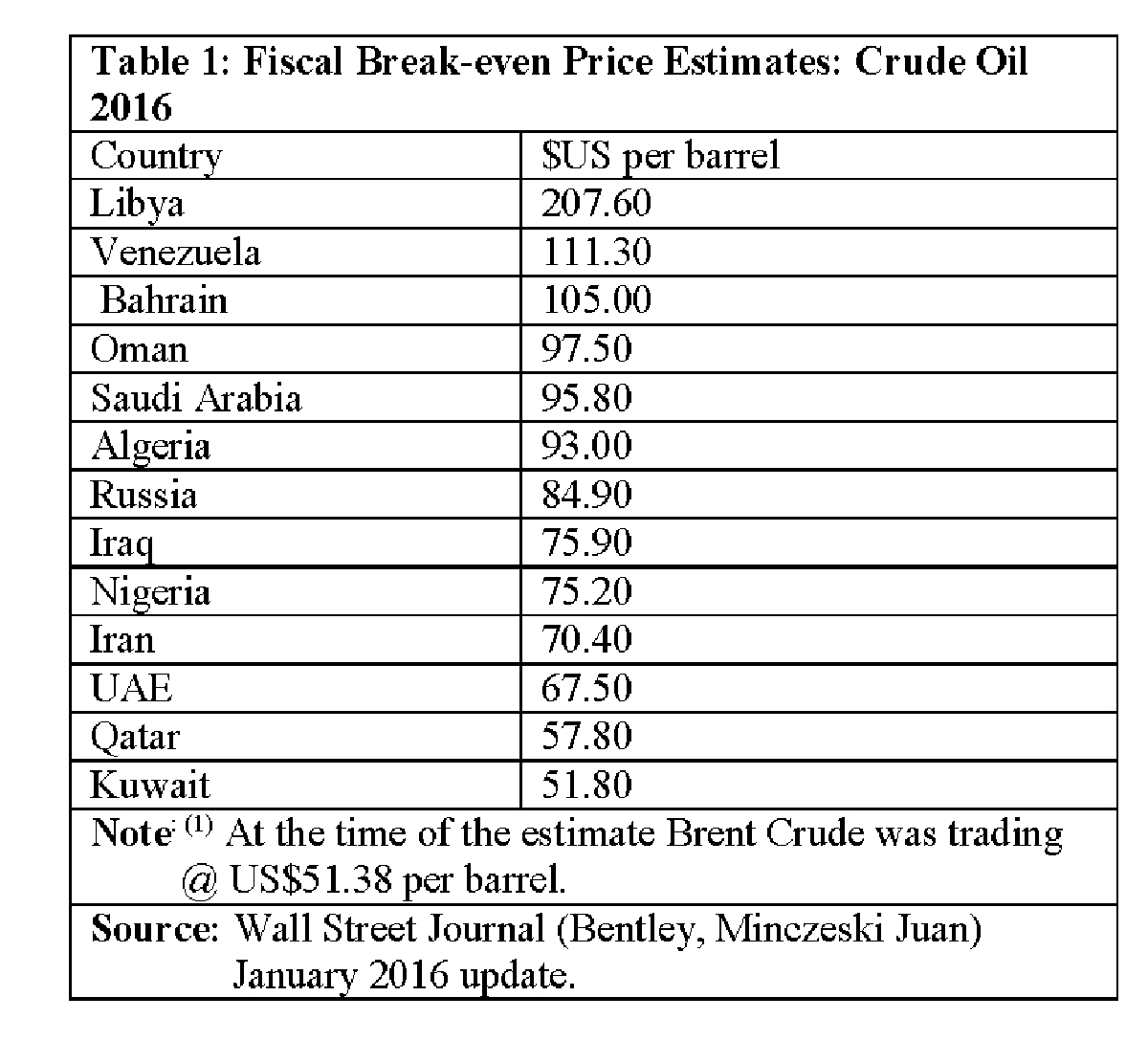

Table 1 provides recent estimates of fiscal break-even prices for a sample of thirteen of the top 20 crude oil producers/exporters. The data reveal there is a wide national variation in these prices. Thus, the range is from US$51.80 (Kuwait) to as much as US$207.60 (Libya) per barrel.

All the fiscal break-even prices shown on the Table exceed the Brent crude oil price of US$51.38 per barrel (see note) prevailing at the time these estimates were published (January 2016). The average for the fiscal break-even prices shown is US$92 per barrel.

Two weeks ago (November 13, 2016), this column had cited data on market determined break-even prices for the ten major crude oil producing regions. The range in that data is from US$27 to US$75 per barrel. It should be noted all of these regional commercial break-even prices are below the average value of the fiscal break-even estimates (US$92).

And, perhaps more strikingly, the range in the market determined break-even prices for the Middle Eastern producers is revealed as US$27 to US$47 per barrel. These estimates are therefore all below the value of the fiscal break-even price estimates, as indicated in Table 1.

Estimation difficulties

In practice, fiscal break-even prices are difficult to determine, mainly because they are normative values. Such values require estimation of the policy targets and outcomes governments are expecting, going forward. And, in the best of circumstances, this requires value judgements which, more often than not, even those in government cannot determine with an acceptable degree of confidence. Not surprisingly, therefore, the estimates that are available vary significantly, when examined by the source of their estimation.

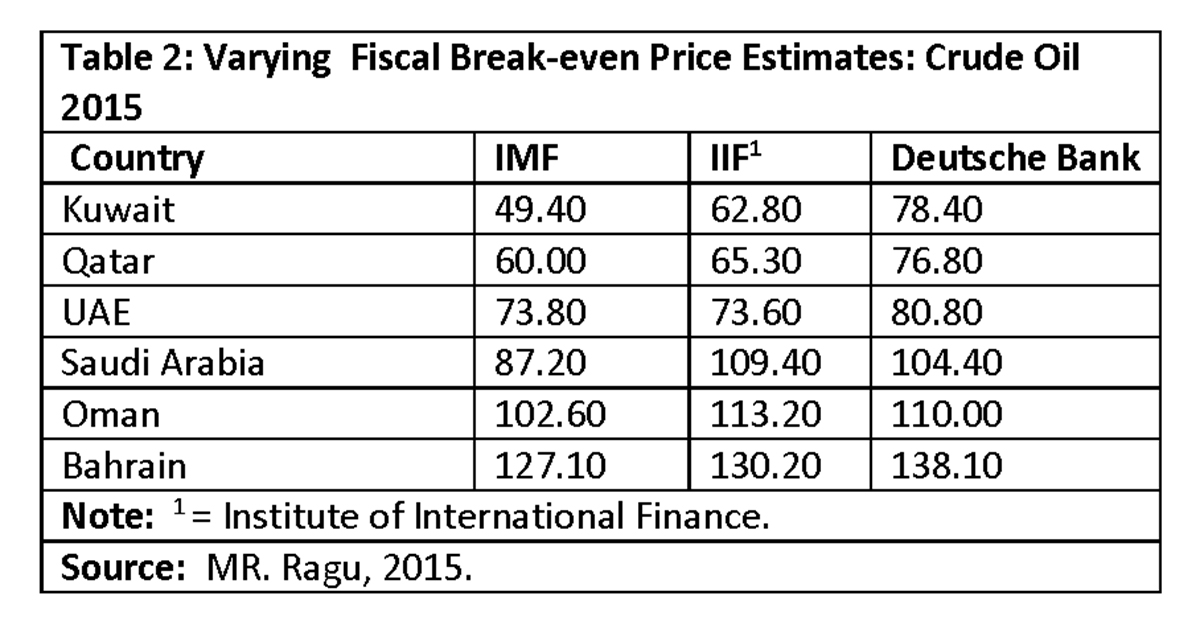

Table 2 highlights this phenomenon clearly, there fiscal break-even prices for six OPEC oil producers are provided. These prices were estimated in 2015; by the IMF, the Institute of International Finance (IIF), and Deutsche Bank. As the Table reveals not only do these estimates vary by country, but also by institution.

While, as a general rule, analysts might claim the estimates provided by the IMF have lower values in the Table, the variation by institution is nevertheless quite marked in several instances. Thus, for example, Kuwait’s estimate varies from a low of US$49.40 (IMF) to a high of US$78.40 (Deutsche Bank), a significant difference of over 50 percent.

In practice though, the estimates provided by the IMF have been treated by analysis as the most definitive. However, if one were to examine the IMF’s estimates of fiscal break-even prices in recent years (as I have done) one would notice significant variation in these estimates, by way of revisions. Indeed some analysts have pointed out that this variation has exceeded 25 per cent in periods of less than one year.

Methodological problems

There are severe methodological issues confronting these fiscal break-even estimates, including: 1) Variance between actual and projected crude oil production and exports; 2) variance between planned and actual government spending; 3) unexpected changes in national exchange rates, which impact on the value in local currency of the normally US dollar denominated fiscal break-even prices; 4) effects of economic, political, social, and other shocks (including natural and man-made disasters; 5) Differences in data provided by ‘official sources’ and those from independent or international sources. Added to such methodological concerns are those which accompany all forecasting: suspect datasets; differences in forecasting techniques; and weak (error prone) analysis.

Conclusion

The above criticisms are not to be taken as an indication that I do not find estimates of fiscal break-even prices useful, and specifically for Guyana. To the contrary, I believe that: 1) such forecasts can be improved (and perhaps even significantly); 2) such improvement is essential if fiscal break-even analysis is to serve as a major tool for strategic decision- making in planning and national budgeting for Guyana, as the country goes forward.

Before I move on to the next topic in this series (hopefully in the next column) I shall first wrap-up this discussion in next week’s column by paying brief attention to two topics. First, a summary indication of the technical/conceptual limitations of break-even analysis. This will be done so as to ensure that readers have an accurate grasp of both the usefulness and limitations of fiscal break-even analysis.

Second, like all such measures in financial analysis, there remains room for improvement. And, as Guyana proceeds in this direction it should seek to advance the usefulness of its fiscal break-even estimates, by taking on board current experiences relating to the limitations of this concept.