The oil contract contains a loophole that may tempt the oil companies to get around the 14.25% of revenues minimum limit cited by some analysts. The only guarantee is the 2% royalty, but the 50%/50% profit share can be exploited such that Guyana’s average take is less than 14.25% in earlier periods.

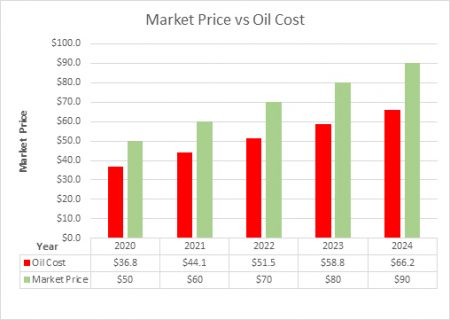

In the graph below, I show a hypothetical 5 years of oil production. In the graph, the price of oil increases from US$50 to US$90. According to Prof Khemraj’s equation, the contract allows for the oil cost to go from about US$37 to US$66 as the price of oil rises. The market price of oil has no bearing on the production cost of oil.

In 2020 the cost of oil per barrel is about $37 but then it rises. This results in the average production cost of oil over this 5-year period being US$51.50. But, if it was profitable to pump at $37 then the average cost over the 5 years should be $37 or lower.

We do not know what the price of oil would be in the future. But if history is a guide, we know that oil prices will fluctuate wildly. Over the last 10 years, the price of oil had fluctuated between above US$140 and below $30. What would prevent the oil companies from ramping up oil production when the market price for oil is low and decreasing it when the oil price is high? The equation shows this would be optimal for an oil company. The oil that is pumped when the market price is low can be stored for sale when the price inevitably fluctuates above the price at which it was originally pumped. In this scenario, Guyana’s profit share would be kept to a minimum to the benefit of the oil companies.

As per the recommendation of the IMF report (commissioned by the government) there should be a ring-fencing arrangement such that the cost from oil fields under production are not allocated to those not yet in production.

As many articles in the press have pointed out, we didn’t get a fair deal from the contract. How can we trust that the oil cost would be allocated fairly?

Darsh Khusial, April 7th, 2018