on tax payments on behalf of oil companies")

Guyana is responsible for paying the interest on the oil companies’ loans. This fact is buried in the Production Sharing Agreements (PSA). (Stabroek Block PSA, Annex C Section 3.1 part (l)). The interest rate to be paid is loosely noted as “market rate”. This flaw may cost Guyana billions of US dollars. It takes just over a billion US dollars to run the country every year. We cannot afford this mistake.

Why would Guyana agree to pay interest on loans that the oil companies negotiated with their bankers is puzzling?

Why would the oil companies want to avoid giving a precise meaning to “market rate”? One has to take note that the interest expense on oil company loans are part of cost recovery. (Up to 75% of oil revenue is set aside for Cost Recovery).

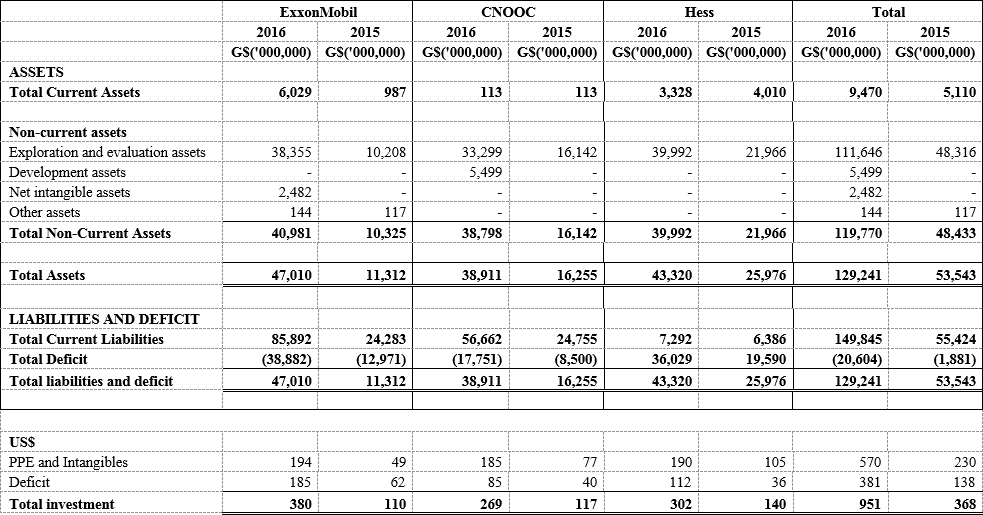

If you scan the Exxon Mobil Financial Reports, you would notice that Exxon has a credit rating of AA+. The credit rating gives you an indication of how safe it is to loan money to a company. Exxon has gold standard credit rating, on par with that of U.S. govt. That is if you loan Exxon money you are guaranteed to get your money back with all interest owed. The market rate on currently traded Exxon loans are about 2%.

Liza Phase 1 has a projected gross capital cost of US$3.7 billion and Liza Phase 2 has a gross capital cost of US$6 billion – with total combined production estimated at 1.05 billion barrels of oil. One should observe that going from 450 million barrels in Phase 1 to 600 million barrels in Phase 2 increased the capital cost per barrel by 20%. However, one would expect, given the lessons learned from the first project, the cost per barrel for the second project should be less than the first. Instead, the difference in cost adds up to an additional US$1 billion!

Let’s scale up the capital cost up to the currently confirmed 6 billion barrels: That would mean the projected capital cost could be US$55 billion or more given the anomaly noted in the previous paragraph.

If we have a company like Exxon that is able to borrow money at low rates then the ‘market rate’ charged to Guyana should be low?At 2% interest, Guyana would be paying US$1.1 billion per year on a US$55 billion loan. If we used ‘Agreed Interest Rate’, defined in the PSA, at present that would be about 3% higher than Exxon’s market. The interest would be US$2.8 billion. That would mean an extra US$1.7 billion going to Exxon instead of Guyana. But ‘Agreed Interest Rate’ was not use in Annex C where it was noted Guyana would have to pay the interest on loans taken out by the oil companies.

Would Exxon argue Guyana needs to pay the market rate similar to that of small and risky oil companies?

Here is the catch. PSA was not signed with the AA+ rated Exxon but with Esso Exploration and Production Guyana Limited (Esso). Esso is a company with negative equity. Negative equity means if you liquidate all your assets you still won’t be able to pay-off your current loans. Thus ‘market rate’ (market interest rate for loans) that Guyana would be paying is not what would be charged for Exxon’s loans but Esso’s.

It may be highly unlikely Esso, a company registered in Bahamas and with negative equity, would be able to receive a loan in the market. This is where Exxon can leverage its low borrowing rate to its advantage. In a typical scenario with the big oil companies, Exxon can loan Esso the money. But what would be “market rate” charged to Esso?

Well, we should look at some of the small and risky oil companies to get an idea. One such company is California Resources, its debt currently pays a market rate of 30%. Another is Weatherford International, its debt currently pays a market rate of 18%. That is a big difference from 2% market rate on Exxon debt.

What would a 15% difference in market rate mean on US$55 billion? That would be an extra US$8 billion going to the oil companies instead of to Guyana. What about a 30% difference? That would be US$16 billion going to the oil companies instead of to Guyana. Now, that sleight of hand not to use the ‘Agreed Interest Rate’ in a section titled “Costs Recoverable Without Further Approval of the Minister“ – doesn’t seem accidental but carefully planned by the oil companies.

Bottom Line: Guyana is stuck not just with paying loans negotiated by the Oil Companies – but at gouging market interest rates. Could this be an US$8 or $16 billion mistake buried in the contract that officials of GoG overlooked or never read.

Darshanand Khusial on behalf of OGGN

References:

https://www.cnn.com/2019/02/05/investing/oil-companies-bond-market-debt/index.html

https://www.businesswire.com/news/home/20190731005186/en/Hess-Reports-Estimated-Results-Quarter-2019

https://markets.businessinsider.com/bonds/exxon_mobil_corpdl-notes_201616-21-bond-2021-us30231gav41

http://www.chrisram.net/wp-content/uploads/2018/05/2018.05.18_Table1.png

{kind=link}