on tax payments on behalf of oil companies")

Every Man, Woman and Child in Guyana Must Become Oil-Minded – Part 100 – July 8, 2022

Introduction

By a strange coincidence, this 100th. column features the 2021 financial statements of Esso Exploration and Production Limited, the designated Operator and holder of a 45% interest in the Stabroek Block under the 2016 Petroleum Agreement. Esso signed its first such agreement in 1999 with the PPP/C Government as a sole Contractor and a second in 2016 with the APNU/AFC Coalition with Hess (30%) and CNOOC (25%) as added Contractors. Esso holds the remaining 45%. These percentages do not, however, reflect the relative size and influence of the ultimate international parents of these branches. It is no accident that Steve Coll, chooses as the title of his seminal book on Exxon, Private Empire: ExxonMobil and American Power. Its vast annual revenues exceed the economic activities of the great majority of countries and, with implications for Guyana, ExxonMobil’s sway over politics and security is often considered greater than that of the United States embassy in that country.

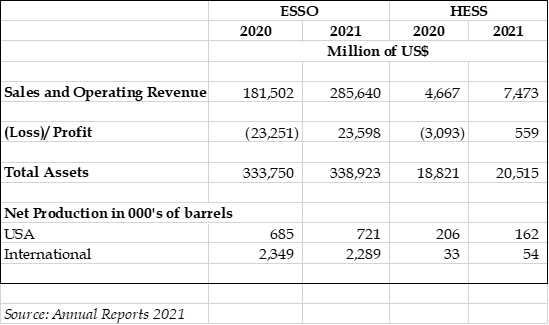

As we did last week in the review of Hess Exploration and Production Guyana Limited for which we did a brief review of its ultimate parent, we will comment briefly on some of the salient features of the annual report of ExxonMobil, the ultimate parent of the local branch operating in Guyana. Exxon is a giant compared with Hess. Here are some performance statistics.

Guyana does feature as prominently in Exxon’s report. But all references are positive. Here are a few:

- Guyana contains one of the largest oil plays discovered in the past decade.

- Exploration success continued with additional discoveries increasing the estimated recoverable resource in the Stabroek block.

- Exxon envisions six projects online by 2027, with the potential for up to 10 projects.

Exxon is probably aware that no legal contortion or high price fiddle will allow them another Petroleum Agreement and that by 2026, the Contractors will have to relinquish all areas other than those covered by Production Licenses issued under the 2016 Production Agreement.

Like Hess, Exxon’s taxes also tell an interesting story. Despite 38% of its revenue being derived from the United States, the US made up only 3.29% of the total federal and non-USA paid by Exxon. And of course, nowhere in the report is there any indication that there are cases where the payment is a paper transaction.

Guyana

Income

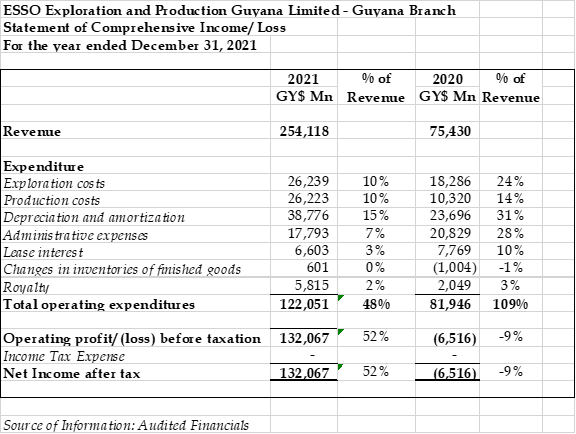

It has been a bumper year for the Guyana branch with revenue of $254,117 million, a growth of 2.4 times from 2020, compared with a growth in revenue of the international parent of 57%. Given the growth in revenue, it is not surprising that all other indicators were substantial improvements over 2020. For example, production cost represents 10% of revenue in 2021 compared with 14% in 2020; depreciation and amortisation has reduced from 31% of revenue in 2021 to 15%; Administrative expenses from 28% to 7%.

Again, we see how our country’s ineptitude allows the oil companies to make a mockery of best practice in petroleum operations as well as in taxation. Here’s the catch: If the GRA was to disallow the exploration costs as not meeting the income tax test of “wholly and exclusively incurred in the production of income”, the taxable profit will actually increase and the amount of tax represented as paid in Guyana will actually increase.

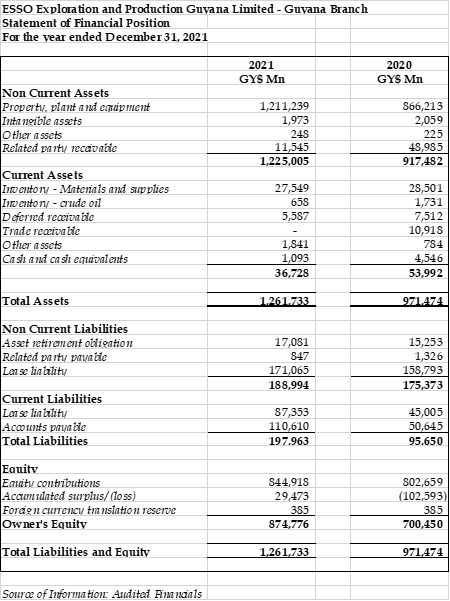

Although not obvious which line item it is charged to, the financial statements carry a note “The amount of restoration obligation includes costs related to petroleum exploration and production activities for decommissioning of floating, production, storage and offloading facility and reclamation of sites.” Some indication is given, however, in the Statement of Cash Flows which show a non-cash charge of $8,754 million as Other long-term obligation provision which is most certainly the de-commissioning provision. If this is in fact a general provision, it should be disallowed for tax purposes, which accrues to the Company’s benefit.

On the question of tax, Esso is in complete denial. The entire report is silent on tax, either as a note, a charge or deferred tax.

Balance Sheet and Cash Flow

The total assets of the Branch, net of depreciation and write-offs, have moved by $290,259 million to $1,261,733 million. Of this total, Property, Plant and Equipment accounts for $1,211,239 million or 96%. The major additions to this class of assets were $319,678 million in work-in-progress for Wells and facilities and $75,477 million in leased Drill Rig assets. Other significant items of assets are Related party receivable of $11,545 million and Inventory – Materials and Supplies of $27,549 million representing drilling of 2021 exploratory and development wells. There is an amount of $5,587 million of Deferred receivable, representing cash call bookings, net of joint billing costs.

The branch started the year with $4,546 million and ended with $1,092 million, despite a $251,198 million being generated from Operating activities. Lease interest paid amounted to $6,603 million while the principal repayment of lease obligations amounted to $7,236 million.

Committed capital expenditure over the next three years is $235,706 million, compared with $359,941 million stated in the 2020 financial statements. Despite the plans announced in the Parent’s report of several wells, for the next few years, the pattern of expenditure shows capital expenditure commitments as follows:

Next week: a round up and commentary on these financials.

Link to Original Article: https://www.chrisram.net/?p=2322